RETIREMENT PLANS FOR STARTUPS

401(k) plans that can grow with your startup.

Help build a people-first culture. Offer an affordable 401(k) plan to help attract and retain top talent.

Retirement plans are complex. Let Human Interest guide you.

Our team of experts will help maintain and operate your startup retirement plan.

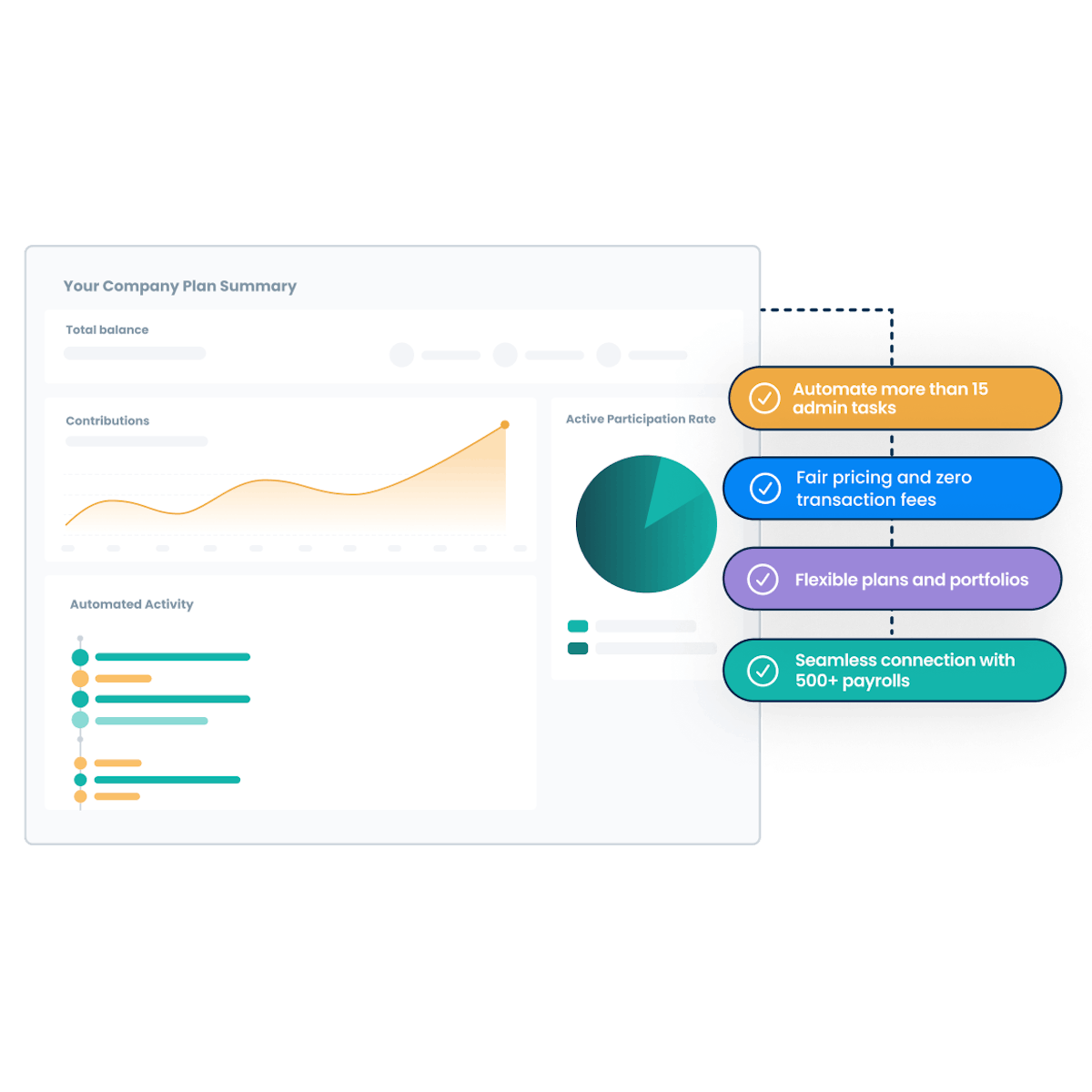

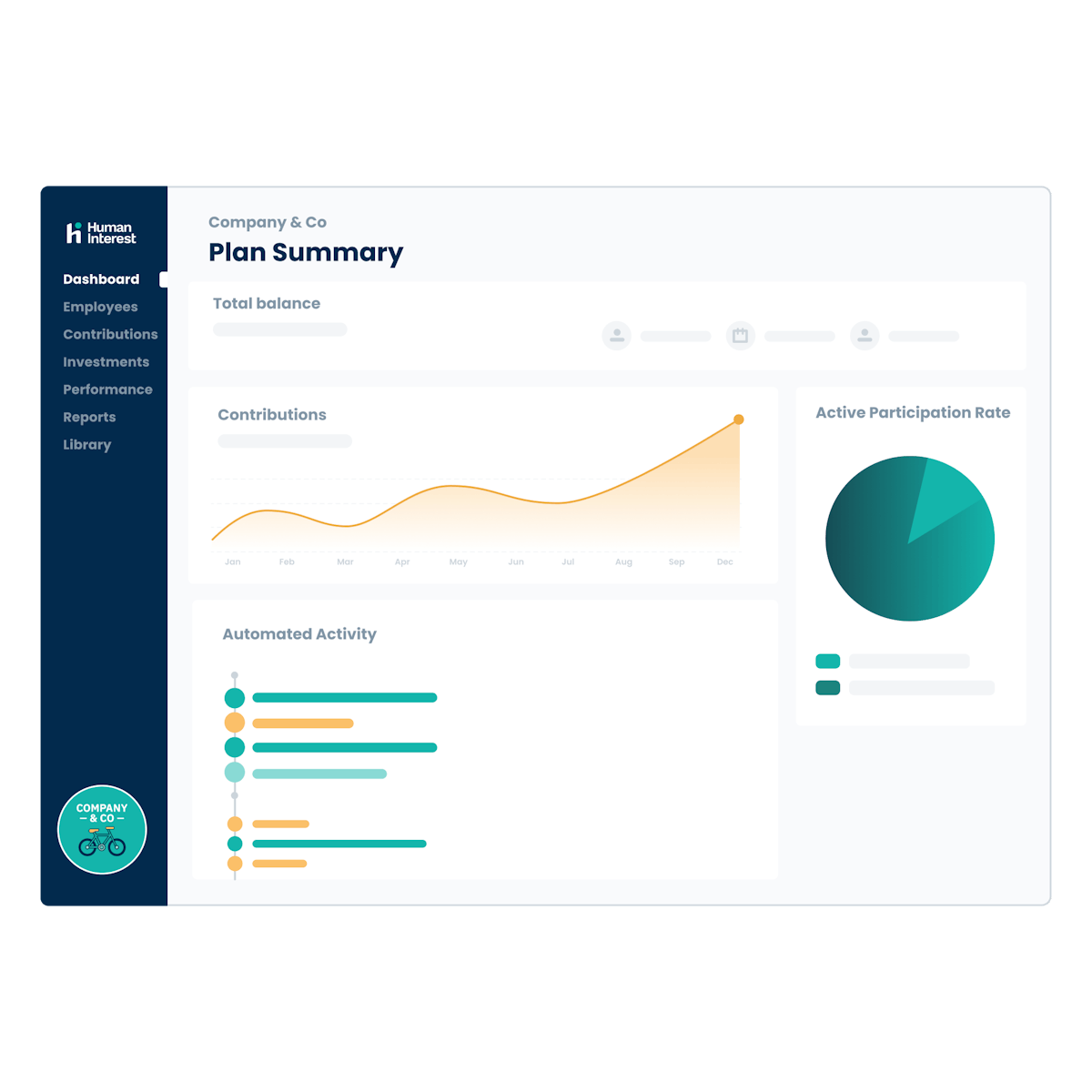

In-house recordkeeping

Automated plan administration tracks participation, contributions, distributions, and more.

Regulatory support

We reduce fiduciary liability by preparing select government filings. And for some clients, we sign and file the Form 5500.1

On-demand reporting

Get a 360-degree view of your plan, access reports, and see which employees have joined.

Plan compliance & testing

Don’t stress about IRS testing and regulatory deadlines. We’ll help handle them for you.

The SMB 401(k) with the most payroll integrations2

Help take the burden off your HR team. We sync with 500+ payrolls to help streamline administrative tasks.

401(K) BUILT FOR GROWING TEAMS

Focus on running your startup. We’ll help with your retirement plan.

Designed to be easy to use. Flexible plan design allows you to customize eligibility and add employer match options.

Reduce manual work. In-house recordkeeping and ERISA compliance—plus select 3(16) fiduciary services depending on your plan.

Help drive employee loyalty. A Human Interest study found that a retirement plan is the most-wanted benefit, after health insurance.3

A 401(k) may be more affordable than you think.

Get a customized, full-service retirement plan with transparent pricing - and zero transaction fees.

Monthly pricing starting at only:

base fee

per eligible employee

An investment advisory fee is paid to Human Interest Advisors (HIA) of 0.01% of plan assets and a separate fee for recordkeeping services and custody-related expenses is paid to Human Interest Inc. (HII) of 0.05% of plan assets. Both fees are deducted on a monthly basis from the employee's account according to the HII and HIA Terms of Service. All prices are exclusive of applicable taxes. If the plan sponsor elects to hire an external investment advisor, the plan sponsor will pay such advisor as agreed between the plan sponsor and advisor. For more information, please see our pricing page.

Help your team save for the future

Give your employees the 401(k) they deserve

Sign up in minutes. Employees can sign up online—or on their phones—in less than five minutes.

Flexible investment options. Employees can choose model portfolios that automatically rebalance—or build their own lineup.

Built-in education. Enrollment webinars and online resources help your team get the most from plans.

Being able to launch a great benefits package and then not give it a second thought was just what we needed. It allowed us to focus on what mattered.

Alison Hunter

Head of People Operations at CloudTrucks

Human Interest solicited clients for testimonials. Active solicitation may make a customer more likely to portray Human Interest favorably. Testimonials are unique to an individual, may not be representative of the experience of others, and past success does not guarantee future results.

MAXIMIZE TAX SAVINGS FOR YOUR STARTUP

A 401(k) may mean additional tax credits for startup employers.

Employers may be eligible for tax credits of up to $5,000/year for three years for setting up a new 401(k) + $500/year for three years for setting up auto-enrollment.4

Resources for startup employers

Investment philosophy

Employees can access mutual funds in every major asset category.

Starting a 401(k) plan

Discover how small business owners can start and manage a 401(k) plan

Payroll integration benefits

Integrate your payroll and 401(k) plan for automation, efficiency, and compliance benefits.

Clear, affordable 401(k) pricing

Customized retirement plans start at $120 per month + $5 per employee per month

Get Started401(k) for startups

frequently asked questions